Update 18 of SEDPI’s Rapid Community Assessment (RCA) October – December 2022

As the world slowly recovers from the pandemic, the economic landscape remains uncertain, especially for nanoenterprises. A recent survey conducted by our organization, Social Enterprise Development Partnerships, Inc. (SEDPI), reveals that 99% of nanoenterprises have resumed operations as of December 2022, indicating a promising recovery for this crucial sector of the economy.

Despite the positive news, recovery remains fragile with 52% of nanoenterprises surveyed experiencing weak demand. Access to supplies has been a continuing concern with 27% of nanoenterprises still reporting difficulties in obtaining the necessary supplies.

SEDPI’s latest self-rated poverty survey reveals that the impact of the pandemic on poverty levels remains significant. For 2022, 54% of respondents rated themselves at the poverty line, a decrease from 81% in 2021. The number of respondents who rated themselves as poor is steady at 3% and 4%. On a positive note, the number of respondents who no longer consider themselves poor nearly tripled from 16% in 2021 to 41% in 2022.

According to the Social Weather Stations, which conducts the survey at the national level, self-rated poverty was recorded at 48% in 2021 and 51% in 2022. The considerably elevated self-rated poverty at the national level suggest that a greater number of nanoenterprises that SEDPI serves experienced better economic conditions.

Over the past three years, SEDPI has conducted an impact assessment to evaluate its support for nanoenterprises through self-evaluation or perception surveys. The results are as follows:

Dec 19

Dec 21

Dec 22

Help in growing business

82%

100%

98%

Education of children

70%

85%

98%

Improve housing

67%

99%

98%

Improve nutrition

81%

100%

100%

Increase income

82%

100%

97%

The perception survey suggests that SEDPI’s assistance plays a crucial role in alleviating hardships among nanoenterprises in areas such as business growth, education, housing, nutrition, and income. This may be the reason why the highly significantly lower self-rated poverty data among SEDPI nanoenterprises compared to the national survey. Additional interventions and strategies in the areas of disaster risk reduction, housing and health are necessary to enable a more comprehensive and lasting escape from poverty.

The majority of respondents are nanoenterprises (45%), owned and operated by women, with an average age of 43 and 73% being married. Of these nanoenterprises, 40% rely on other sources of income, such as employment, while 12% are unpaid family members, and 2% are unemployed.

SEDPI is a microfinance institution dedicated to providing ethical financing to nanoenterprises in Agusan del Sur, Davao de Oro, Davao del Norte, and Surigao del Sur. Their efforts have led to significant improvements in various aspects of the beneficiaries’ lives, such as business growth, education, housing, nutrition, and income.

The COVID-19 pandemic has had a profound impact on nanoenterprises (NEs) worldwide, with various stages of recovery, demand trends, and access to supplies experienced throughout the course of the pandemic. This article examines the chronological analysis of NEs’ recovery, demand trends, and access to supplies from March 2020 to December 2022, based on the Rapid Community Assessment conducted by the Social Enterprise Development Partnerships, Inc. (SEDPI). By analyzing these trends, we can better understand the challenges faced by NEs and the factors contributing to their resilience and adaptability.

March 2020: Initial Pandemic Impact, Demand Shift, and Supply Chain Disruptions

At the beginning of the COVID-19 pandemic in March 2020, 34% of NEs stopped their operations due to lockdowns and social distancing measures, while 66% resumed operations. Demand was characterized by 8% of NEs experiencing no buyers, 78% experiencing weak demand, and 13% witnessing strong demand, as consumers’ priorities shifted towards essential goods and services. Supply chain disruptions affected NEs, with 36% facing difficult access to supplies and 64% having access to necessary resources.

June 2020: Early Recovery, Persistent Weak Demand, and Supply Chain Struggles

In June 2020, the recovery of NEs continued, with 91% resuming operations and only 9% remaining closed. However, demand remained weak, with 7% of NEs having no buyers, 72% facing weak demand, and 21% enjoying strong demand. Access to supplies was a significant challenge, as 81% of NEs had adequate access while 19% faced difficulties due to ongoing supply chain disruptions caused by the pandemic.

December 2020: Relief, Recovery, Improved Demand, and Better Supply Access Amid Typhoon Vicky’s Impact

By December 2020, government relief packages and easing of lockdown restrictions helped many NEs recover, with 3% remaining closed and 96% resuming operations. Demand improved slightly, with 4% of NEs having no buyers, 75% facing weak demand, and 21% enjoying strong demand. The holiday season likely contributed to increased consumer spending. Access to supplies significantly improved, with 90% of NEs having access and only 10% experiencing difficulties.

However, during this period, Typhoon Vicky hit the region, causing agricultural production losses in rice, corn, high-value crops, and livestock. The typhoon also triggered floods and landslides, resulting in damaged or destroyed homes in coastal areas. The natural disaster added challenges to the recovery process of nanoenterprises, particularly those in the affected areas and those dependent on agricultural production. Although the overall trend in December 2020 indicated progress in recovery, improved demand, and better access to supplies for nanoenterprises, the recovery would have been even more significant if not for the added challenges brought about by Typhoon Vicky.

March 2021: Steady Recovery, Increased Strong Demand, and Improved Supply Access

By March 2021, the situation for NEs had improved, with 97% resuming operations and only 3% remaining closed. Demand patterns shifted, with only 1% of NEs having no buyers, 52% experiencing weak demand, and 47% enjoying strong demand, likely due to the easing of restrictions and ongoing vaccination campaigns. Access to supplies improved, with 73% of NEs having adequate access and 27% still facing difficulties.

June 2021: Full Recovery, Diverse Demand, and Enhanced Access to Supplies

By June 2021, 100% of NEs resumed operations, marking a full recovery in this period. Demand varied, with 2% of NEs having no buyers, 64% facing weak demand, and 34% experiencing strong demand. Access to supplies continued to improve, with 82% of NEs having adequate access and only 18% facing difficulties.

September 2021: Delta Variant Surge, Granular Lockdowns, and Nanoenterprise Adaptation

In September 2021, the Delta variant surged in the Philippines, prompting the government to implement granular lockdowns as opposed to the general lockdowns previously imposed. This new approach aimed to prevent the wholesale disruption of jobs and livelihoods while still addressing the public health crisis. Despite the surge and the implementation of granular lockdowns, 96% of NEs continued to operate, while only 4% temporarily stopped their operations.

Demand patterns during this period fluctuated, with 12% of NEs having no buyers, 66% experiencing weak demand, and 22% witnessing strong demand. As the granular lockdowns targeted specific areas with high infection rates, many nanoenterprises had to quickly adapt to the changing circumstances and market conditions. Access to supplies remained relatively stable, with 77% of NEs having adequate access and 23% facing difficulties.

The September 2021 period demonstrated the resilience of nanoenterprises in the face of new challenges posed by the Delta variant and the government’s shift in lockdown strategy. Despite the hurdles, the sector continued to adapt and maintain its operations, contributing to the nation’s economic recovery.

December 2021: Continued Recovery, Increased Strong Demand, and Moderate Access to Supplies

By December 2021, widespread vaccination campaigns allowed for more relaxed social distancing measures and a resurgence in consumer demand. The percentage of stopped NEs remained at 3%, while 97% resumed operations. Demand for NE products and services further improved, with 9% of NEs having no buyers, 65% facing weak demand, and 26% experiencing strong demand. Access to supplies became more moderate, with 77% of NEs having access and 23% facing difficulties.

March 2022: Steady Operations, Persistent Weak Demand, and Improved Access to Supplies

By March 2022, the status of operations remained consistent, with 4% of NEs stopped and 96% resumed operations. Demand continued to lean towards weakness, as 8% of NEs had no buyers, 67% faced weak demand, and 26% experienced strong demand. However, access to supplies significantly improved, with 85% of NEs having access and only 15% facing difficulties.

September 2022: Temporary Setbacks, Fluctuating Demand, and Slightly Reduced Access to Supplies

In September 2022, the temporary increase in stopped NEs to 4% could be attributed to localized outbreaks and new COVID-19 variants. Despite these setbacks, 96% of NEs remained operational. However, demand patterns fluctuated, with 15% of NEs having no buyers, 36% experiencing weak demand, and 49% witnessing strong demand. Access to supplies slightly declined, with 73% of NEs having access and 27% facing difficulties.

December 2022: High Inflation Impact on Nanoenterprises, Demand Patterns, and Purchasing Power

In December 2022, the Philippines’ headline inflation increased to 8.1 percent, as reported by the Philippine Statistics Authority (PSA). The high inflation rate led to a decrease in purchasing power, resulting in reduced consumer spending, particularly among low-income households. Despite the inflationary pressures, 99% of NEs remained operational, while only 1% stopped their operations, showcasing the resilience of the sector.

Compared to September 2022, when 36% of NEs faced weak demand, the percentage increased to 52% in December 2022, illustrating the heightened challenges for these enterprises due to reduced consumer spending amid high inflation. The decreased purchasing power of consumers, especially in low-income households, contributed to the fluctuations in demand patterns for nanoenterprises.

Access to supplies remained relatively stable, with 73% of NEs having access to necessary resources and 27% facing difficulties in acquiring them. The December 2022 period highlighted the challenges faced by nanoenterprises due to high inflation and its impact on consumer spending, while also demonstrating the adaptability of the sector in sustaining operations amid economic challenges.

Conclusion:

Throughout the COVID-19 pandemic and various external challenges, such as natural disasters and high inflation, nanoenterprises have consistently demonstrated resilience and adaptability in maintaining operations, responding to fluctuating demand, and navigating supply chain disruptions. As of December 2022, the sector has reached a near full recovery, with stabilizing demand patterns and steady access to supplies. The findings from SEDPI’s Rapid Community Assessment underscore the importance of continued support and empowerment for nanoenterprises, as they play a crucial role in local economies and communities. As the world moves forward from the pandemic’s impact, fostering collaboration between government, business, and community organizations will remain vital in ensuring the sustained success and growth of nanoenterprises in the face of ongoing and future challenges.

Respondents:

In December 2022, the Rapid Community Assessment (RCA) conducted by SEDPI garnered responses from 1,398 respondents across the provinces of Agusan del Sur, Davao de Oro, Davao del Norte, and Surigao del Sur. The profile of respondents in this edition of the survey was similar to that of previous editions. The majority of respondents were female (86%), with an average age of 43, and 73% of them were married. When it came to sources of income, 40% were employed, 45% were nanoenterprise owners, 12% were unpaid family members contributing to the family business, and 2% were unemployed.

Ms. Mary Jane Selecia, sari-sari store owner in Manguindanao, Philippines.

Mary Jane Selecia is a mother of five who lives in a rural community in Upi, Maguindanao in the Philippines. She runs a sari-sari store (corner store) in her community. COVID-19 has significantly affected their household and community.

To mitigate the spread of COVID-19, the government imposed community quarantine measures which includes physical distancing, movement restrictions, suspension of classes, and conduct of awareness campaigns on infection, prevention, and control measures (IPC). To cushion the socio-economic impact of the quarantine, subsidies were provided to households to complement their existing resources.

The government subsidy reminds Mary Jane that her household needs to maximize their savings. “My shop is bringing in one-third of the profit. I would earn around P4,000 (US$ 82) and now I am fortunate if I make P1,000 (US$20) a week. We invest P3,000 (US$ 61) a week just to keep the store running,” she said. Their household requirement for a month is estimated at PhP 9,000 (US$ 185) and was previously covered from the sari-sari store’s profits.

Borrowing money is becoming a vicious cycle for Mary Jane, “We have no savings and the income we make for our businesses go towards repaying our loans from relatives and friends. It seems like we are borrowing to pay over and over again,” she said.

Relief information is even more scarce when in the remote mountainous areas like Tinungkaan. The interventions in Mary Jane’s town were constrained to the Department of Social Welfare and Development (DSWD) conducting a survey to determine the poorest population in the village.

Mary Jane’s husband works as a Barangay Secretary and his work became an unexpected lifeline, “We did not need to apply for the Social Amelioration Program (SAP) because of my husband’s job. We are also beneficiaries of the Pantawid Pamilyang Pilipino Program (4Ps),” she explained.

The SAP has given qualified families P5,000 to P8,000 per month for two months. “We bought one sack of rice. The remaining money is additional capital for our store,” she said.

Farming has augmented the dwindling income of the household. “Our alternative sources of income are planting vegetables and raising farm animals. The small farm supports us while providing us with food. We are often forced to consume supplies from the sari-sari store,” she explained.

Stock in her store is already limited because of the limited supply in Noro, where she buys her supplies. Transportation cost for each of the trips to Noro is now P100, which is an exacerbated cost during the lockdown.

Everyday expenses have become a challenge for her community. “There is a decline in sales because many of our neighbors and customers do not have work,” she said. As the COVID-19 situation evolves, Mary Jane adapts to provide food on the table for her children and access to basic commodities in her community.

This case study on the plight of microenterprises in the Philippines was selected for the International Day for Rural Women (15 October 2020). It was originally shared across the Asian Disaster Preparedness Center (ADPC) platforms for the International Day for Rural Women

Federic Caneta / Resident of Cebu City – Furniture Maker

The miter saw is silent in Federic Caneta’s workshop. The carpenter has a cabinet and a couple of shelves from commissions that were canceled because of the lockdown. His monthly projects vary with demand, “I make furniture on a custom-made or pre-order basis. Orders would range from P8,000 to P15,000 a month. There has been no demand since the enhanced community quarantine.” His daughter, Rica Caneta, is a private school teacher. She has been helping him sell some of his works, “I made a hanging cabinet and a storage cabinet with the extra wood from the previously commissioned projects. I sold them for P2,500 and P3,000 respectively. Rica is working from home so she takes some time to promote my pieces through social media.” The average monthly salary for a carpenter is P16,800. Profits come from down-payments upon the order or balance payments upon delivery. Federic is concerned that he might not have supplies to continue the few online sales, “I had one piece that I was not able to complete. I was unable to obtain the needed materials due to travel restrictions. Some customers have also canceled their orders.”Federic’s son, Drake, is an animal handler and is supporting the family through these times, “My children are providing financial support we need. Our monthly expenses are usually P10,000 which was primarily covered through my business.” He has discovered the potential of taking his business online to help it grow, “I would need around P10,000 to buy materials for future orders. Online sales have made me realize that professional guidance in promoting our business would really help it expand.”

Chierrie Villarosa Marces / 29 years old / Resident of General Santos City- Pisonet

When life gives you the Internet, make digital solutions for your business. Chierrie Villarosa Marces owns a small Pisonet (pay-by-the-minute computer and Internet shop). The lockdown has forced her to close her shop so she is selling goods through digital networks, “I have closed the pisonet since mid-March. I am focusing on online trading which includes buying and selling dry goods, food items, and other basic commodities.”

Online sales are the only means of income for Chierrie, “I make around P200 for every P1,000 I invest in online selling. I have been doing it for some time but even that has experienced a decline.” Her customers have stopped ordering dried foods, “Basic goods and essential commodities such as fruits and cooking ingredients are the priority now. We own a tricycle that we use to transport orders. Travel restrictions have made getting the goods from my supplier difficult.” However, these sales do not provide stability for the pisonet. Filipinos spend the most time on the Internet around the world, averaging in at 10 hours per day. Her Internet business had expanded to printing, scanning, and photocopying services, “I would make around P25,000 every month from the pisonet. The expenses would be around P8,000 for the Internet and electricity bills. My direct suppliers have been generous enough to offer freebies on their services for now.”

Chierrie is struggling to make ends meet, “Our household expenses are about P10,000 every month. I am grateful to the government for providing us with rice, meat, canned goods, and other staples.” She is worried about restarting the business once the community quarantine is lifted, “I estimate that we will need at least P5,000 to restart the pisonet. It would cover two months of our Internet bill. We can manage the cost of computer maintenance and business equipment.”

John Cuvin / Resident of Naga City – Laundry Shop

John Cuvin, his wife, and his mother are bonded in their dream to be business owners, “My wife owns a beauty salon and my mother has also had a number of businesses.” He established a laundry shop, JJS Suds Laundry Service as a lucrative business opportunity. Dry cleaning and laundry services ranked second in the service industry, providing business opportunities for 18% of entrepreneurs. John’s monthly expenses amount to P25,000 as he provides support for his family, “My wife and mother live in different provinces and I would pay for their utilities and my mother’s caretaker. I want to provide them with financial support.”

JJS Suds is a connection to the local community, “We would normally have 30 to 50 customers a day before the lockdown. We are lucky if there are five customers these days. Our daily revenue would reach up to P15,000 per day and that target is now P5,000.” John has had to cut corners to adapt to the new normal, “We had seven workers on a daily basis and now there are only two at any given time. The store is only open for limited hours because customers no longer come in late at night. It has led to slower service delivery. We have also started using electric fans.”

Basic supplies have become much harder to procure. His team promotes the use of dryer sheets when the fabric conditioner is short on supply- “Wholesalers have increased the price of fabric conditioner and liquid detergent from P10 to P11 per sachet. Sometimes we have to buy them from the local retailers for P17. The dryer sheets would be available for P500 per box but they are not locally available. We sell each sheet for P10.”Communication is a constant with John’s regular clientele. The staff coordinate with customers on Facebook. John has also decided to bring the business to his regulars, “We also support our personnel needs by helping with the laundry and delivery. The shop currently relies on delivery modality to remain operational. Finding alternative solutions is necessary to keep the business running.”

Although business expenses were high, John would earn between P30,000 to P50,000 a month, “I spent around P120,000 which included the P50,000 for my staff’s salary on a monthly basis.” He anticipates support or policies in order to relieve the challenges they are facing, “It would be really helpful if the government could provide financial support to cover the salaries of our staff, and postpone rent collection or allow us to pay it in installments.”

Pureza Elopre Granario / Resident Naga City – Sari-sari store

Opening Pureza’s shop is necessary for survival but also puts her family at great risk, “My husband and mother-in-law are both over 50. I worry that I might bring the virus home.” Work is scarce for her husband who is a plumber. “We are fortunate that profits from the store are still P800 to P1,000 per day.”

The green and white awning in her shop have been a part of her neighborhood’s fabric for years, “My supplies get sold easily. Before the quarantine, sales were mostly liquor and sodas. Customers now want canned goods and frozen foods which ensure that they can stay at home. Sales of phone credit are always in-demand and have gone up by 20%.” Pureza maintains is systematic when it comes to buying stock for her shop, “We have to go at a specific time and day so that we can avoid the long lines. There is still a queue but any steps we can take to be cautious are necessary.”

A savings and investment scheme supports small businesses from any shock in income flow. Pureza is fortunate to have enough to restart her business. She estimated that P10,000 was enough to restock her full inventory, “I was a part of the Social Amelioration Program (SAP) through which I received P5,000. We used the money to purchase additional inventory for the store.” Her mother-in-law has also contributed to the shop. “She gave me a P2,000 loan which I used to buy coffee, sugar, and soap.”Pureza’s shop is her saving grace during the uncertainty, “We need P9,000 for our household expenses and about P7,000 for the store.” The store is a constant for her. Its history in the community mirrors Pureza’s presence and determination, “We reinvest all of our profits into the shop. I’m obtaining inventory through other channels because I want to see my store grow despite the circumstances.”

At APP, we focus on the vulnerable sectors of our society in our development initiatives. MSMEs are among the priority sectors of our national chapter, Philippine Preparedness Partnership’s (PHILPREP) and its targets in local program activities. PHILPREP has developed these case stories to amplify the voices on the ground, especially during the COVID-19 pandemic. It seeks to amplify human stories to raise awareness on how disasters affect the most vulnerable communities.

This article was developed in partnership with the Asian Preparedness Partnership (APP). More information about APP may be found using this link: Asia Preparedness Partnership (APP).

Click the links for Part I and Part II of this series.

Respondent: JhunRodriguez / Resident of Quezon City- Tricycle Driver

Jhun Rodriquez’s day would start with morning commuters in Quezon City. He is one of 4.5 million drivers across the country who have left their vehicles in garages until quarantine conditions are lifted. Jhun has put a ‘Family Use – Private’ sign on his tricycle, “We are only allowed to use it for business purposes and personal family needs.” The lockdown has banned tricycle drivers from passenger transport since March 15, 2020. “I attempted to take my tricycle the day after the lockdown. The authorities had warned me that it would be impounded. My tricycle is leased so I did not want to take the risk.”

The rent for the tricycle is P200 per day. Jhun had previously earned enough to support the family of 11, “I would usually earn up to P24,000 a month.” Support comes from the family during the worst disasters. Jhun was able to rely on his brother when tropical storm Ondoy ravaged the city in 2009, “My brother is too old to work now so it is my turn to ensure his well-being. I do not have enough money to start a business and our savings have gone towards food and medicine.” Jhun and his brother’s family only eat lugaw, a rice porridge, most of the time. “Eating the same meal every day becomes really difficult for the children. I assure them that when I am able to resume working, we will eat like we used to again.”

The city was distributing P2,000 for tricycle drivers which Jhun was unable to collect, “I believe it is because my house is far from the collection point. The local government did provide us with rice and sardines on two occasions. We have also received grocery items from Gawad Kalinga.” Local organizations have become the most dynamic advocates during the pandemic.

Jhun’s tricycle has become an unexpected business tool: “I was able to borrow P5,000 from my friend and I used the money to buy and sell fish.” He uses the tricycle to take his supply to the local market. “Everyday kindness keeps me optimistic. My customers don’t haggle for lower prices and some do not even ask for their change. It has allowed me to pay back the loan within a week.” Jhun usually buys 20 kilograms of fish and was able to make a profit of P600 per day. Matters have gotten worse since the total lockdown has restricted him from selling at the marketplace.

Respondent: Edwin Cawit / Resident of Lagao, General Santos City – Food delivery service

The onset of social distancing and isolation steadily witnessed a decline in Edwin Cawit’s food delivery service, “We started to feel the effects of COVID-19 in the second week of March when many of our clients canceled their previous orders. Our services came to an immediate halt as of March 18. I understand that safety measures are necessary but the indefinite timelines put us in a dilemma.” His business was growing with profits of P60,000 to P80,000 a month. Although food delivery services make up a small portion of the industry, it has witnessed a steady increase with an expansion of 7.3% between 2016-2017.

Edwin’s passion project has always been on the plates, “I started the business after years of savings because I wanted to be my own manager and operator. Cooking meals was always a family affair so it was a natural career move. I am able to cope because I do not have to compensate for any employee’s salaries.” Edwin has savings to sustain his family but the uncertainty remains a concern. “The only way to prevent fines or penalties was the ‘wait-and-see’ option at the beginning of the lockdown. We listen to and follow updates from our local news outlets and social media pages. We are very careful because our services involve people’s consumption.”Inflation of necessary supplies during a disaster event makes business continuity an even greater challenge. Edwin’s main concern is procuring inventory, “We pick up essential ingredients from outside the local area because of lack of availability. The city’s clustering policy during the lockdown prevents vendors from sourcing some of the vegetables we need from Bukidnon.” The scarcity in supply and increase in price has forced Edwin to shut down despite being able to operate under COVID-19 safety guidelines. “The price of vegetables has inflated by 20 to 30%. Rice and grains have only gone up 10%. However, these cumulative prices make it impractical to continue operations.” The emerging caterer hopes that small businesses will receive the aid they need to carry on after the restriction, “We would appreciate logistical support, availability of supplies from the National Capital Region and other key cities, tax relief, and easing of local cluster market restrictions.”

Respondent: Shirly Erum / Lagao, General Santos City – Driving Instructor

Shirly Erum’s classroom is the road of General Santos City- “I believe that driving is in our blood. Five out of our nine family members are driving instructors.” The school of driving can be a promising career as instructors make an average of P235,451 annually. The number of students started to slow down in March. “We no longer have enrollees because of the transportation restrictions. Physical distancing also makes it impossible to hold practical sessions.” They would offer three package deals – a five day tutorial for P2,800, seven days for P3,800, or a monthly package between P10,000 to P20,000. Keeping their office is the biggest challenge, “Our maintenance cost fluctuates between P5,000 to P10,000 and the rental fee for the office is P7,000. We have used our savings to continue paying the rent and any vehicle maintenance that was necessary.” Shirly also has to consider the family expenses, “My sister works in Hong Kong and has sent us remittance of P20,000 during the lockdown. We were able to use the money for four months of household expenses. If we can resume operations soon, we would only need P5,000 to start functioning again.”

Respondent: Giselle Pastrano / Resident of Cebu City – Self-service Car Wash Business

The Pastranos anticipated that 2020 would be a year of new beginnings and opportunities. Giselle and Arnold welcomed a new baby, Arnold, in April. They had also opened a new business to provide for their growing family. Transforming their garage in front of their home as optimal for starting their venture. Giselle would be able to take care of her family and work, “Our space was large enough to situate a self-service car wash and food stall. We would earn around P9,000 to P12,000 from the car wash and P16,000 to P18,000 from the food stall.” Both businesses had minimal expenses because they were run by Giselle and Arnold, “We would spend P1,000 to P1,500 that was mostly for the water bill. The expenses for the food stall were P9,000 a month. The profits were more than enough to cover the P7,000 we would need for the household.”

They had only been operating for a month when they decided to shut down. Giselle’s immediate concern was her family’s safety, “Our business is in front of the house. Customers coming in and out expose my family. Compromising their health is never an option.” She also has a seven-year older son, Travis, who is currently unable to attend school. The food & beverage industry is expected to reach $415 million by 2024. Food stalls are becoming more popular as the younger generations opt to eat out. “Many of our ingredients have gone up by 40% to 50%. Our regular customers shared the same concerns and we started seeing a decline in customers when the lockdown started.” Commuter restrictions eventually led them to cease operations of the car wash. Multiple income-generating opportunities are a proven solution for many small businesses to sustain their needs. The COVID-19 restrictions have limited these prospects to entrepreneurs. Giselle currently works as a cashier for a university. It is the only stable income for the household. The lack of earnings has forced her to take loans, “My husband has a van that he would use for delivery operations. He would regularly work for Lazada but that has also stopped since March.” Loss of revenue sources has multifold consequences for microentrepreneurs. “We have lost around P19,000 a month since the lockdown. We also had an SUV that we would rent out through the Grab app. Unfortunately, we had to give it back to the dealership because we were unable to cover the monthly payment or the driver’s salary.”

At APP, we focus on the vulnerable sectors of our society in our development initiatives. MSMEs are among the priority sectors of our national chapter, Philippine Preparedness Partnership’s (PHILPREP) and its targets in local program activities. PHILPREP has developed these case stories to amplify the voices on the ground, especially during the COVID-19 pandemic. It seeks to amplify human stories to raise awareness on how disasters affect the most vulnerable communities.

This article was developed in partnership with the Asian Preparedness Partnership (APP). More information about APP may be found using this link: Asia Preparedness Partnership (APP).

Update 10: SEDPI Rapid community assessment on the impact of COVID-19 to nanoenterprises

Two months after the government started easing lockdowns in most parts of the country, 36% of nanoenterprises reported to have bounced back to pre-pandemic level. In May, only 18% expected to bounce back within one month which may be a good sign of recovery if the spread of the virus is contained.

Nanoenterprise (NE) is a SEDPI-coined term that refers to unregistered livelihoods of self-employed individuals. They typically operate informal businesses alone or with the help of unpaid family members targeting their own immediate local communities.

Status of nanoenterprises

Those that bounced back report that they are already able to earn about the same income; and experience normal demand to their products and services. For the month of June, there were twice as many nanoenterprises reporting slowdown in sales compared to those that reported strong demand.

Access to supply on inputs needed to operate their livelihoods remain stable.

Financing options

Nanoenterprises typically access loans from informal sources which make them vulnerable to predatory financing practices. Most of them borrow money from cooperatives, rural banks, microfinance NGOs and pawnshops.

On average, nanoenterprises borrow a small sum of money ranging from PhP3,000 to PhP10,000 to finance their livelihoods such as sari-sari stores, carinderia, farmers, fisherfolks, dressmaking and vending. Microfinance institutions offer collateral-free loans to them payable in three to six months with interest rates ranging from 2% to 5% per month.

With microenterprises cautious on demand, they prefer not to access loans. Only two of three of those who finished their loans opted to renew their for another cycle. This is also a sign that nanoenterprise have the ability to weigh risks and returns.

For the month of June, when normal loan collections resumed, one in three nanoenterprises was able to repay in accordance with amortizations based on the Bayanihan Act’s loan deferment schedule. A majority are requesting for up to two months additional grace period to allow them more time to adjust and cope with the new normal.

Essential financial service to low income group

There are approximately 8 million low income households that access microfinance services in the Philippines. MFIs are frontliners in the delivery of financial services to low income groups who find it difficult to open deposit accounts and access loans from commercial banks.

SEDPI estimates that a PhP40B economic assistance to nanoenterprises channeled through MFIs will address their financing needs to jumpstart their livelihoods. This is based on 8 milion estimated number of microenterprises and PhP5,000 economic assistance package.

The proposed Philippine economic stimulus package contains a total of PhP245 billion budget to assist micro, small and medium enterprises. Only a small fraction of this is expected to reach nanoenterprises.

Prioritizing nanoenterprises

The negative impact of COVID-19 to nanoenterprises is undeniable. The research shows that nanoenterprises are showing positive signs of bouncing back faster.

Preferential option to those at the bottom of the pyramid should be extended first since these groups can bounce back quickly; only need a small amount of stimulus; will reduce need for cash dole outs; and will reach millions of Filipino low income households.

Note:

The research is part of a series of rapid community assessments that determines the economic impact of COVID-19 to microenterprises and the informal sector. SEDPI, a microfinance institution (MFI), conducted the survey from June 23-30 with 5,791 respondents located in Agusan del Sur and Surigao del Sur.

It is not a representative sample of the entire Philippines. It is highly localized but should be a good case study that reflects the situation in the countryside. SEDPI believes that the nationwide experience may not be far from our research results.

Previous updates:

The titles are hyperlinked. Click on the titles to full read article online.

Agrarian Reform Beneficiary Organizations (ARBO) in Sarangani, Sultan Kudarat, Maguindanao, and Lanao del Sur Provinces remain covid free. This is the result of the ARBO covid-19 quick assessment conducted by SEDPI on April 20-24, 2020.

While some ARBOs have completely stopped operations, 36% or ten (10) out of twenty-eight (28) participating ARBOs continue to provide services to farmers in their communities. These services include irrigation, farm machinery rental, catfish culture, animal dispersal, and farm monitoring.

ARBO farmer members still manage their individual farms. However, due to the strict implementation of the community quarantine, senior citizen farmers are unable to do so.

Pambansang Mananalon, Mag-uuma, Magbabaul, Magsasakang Pilipinas, Inc. Farmers Association (P4MP-FA) of Upper Katungal in Tacurong City, reported that they have temporarily stopped their microfinance services since members failed to pay their dues due to the lockdown. At the same time, the farmers’ economic activity is put on hold because of restrictions in selling produce and other goods in the market.

One ARBO in Sarangani, Alkikan Vegetables Growers Association (ALVEGA), continues to consolidate vegetables funnelling it to a local bagsakan and a huge grocery in General Santos City. On the other hand, Upper Biangan Farmers Association (UBFA) who offers micro insurance services has twice provided relief goods and cash assistance to their members. Only three (3) of the twenty-eight (28) ARBOs have received assistance as an organization from their local barangay and municipal government.

During this quarantine period, some ARBO members in Cotabato, Maguindanao, and Lanao del Sur have volunteered in the Bantay Covid initiatives of their barangays by manning border outposts.

SEDPI is a group of social enterprises that provide capacity building and social investments to development organizations and directly to microenterprises. We serve ~8,000 microenterprises in Agusan del Sur and Surigao del Sur, two of the poorest provinces in the Philippines.

Most of our members, about nine in 10, are women with an average age of 42. These women are typically into vending, farming, fishing, dress making, selling food, and livestock backyard raising.

Community assessments

Every week, since the community quarantine was imposed on March 15, 2020; SEDPI conducted community assessment research with its members. These were conducted on March 15, March 30, April 5 and April 14; through rapid survey via text messaging and calls with our members.

The rapid community assessment aims to determine the economic impact of COVID-19 on our members and to have a clearer picture of what transpires on the ground. We asked our members the following:

Status of their livelihood – unaffected, weakened or stopped

Experience symptoms of COVID-19

Access to government assistance

Support needed after the community quarantine

Impact of COVID-19 to microenterprises and informal sector

All microenterprises were negatively affected due to COVID-19. Immediately after the community quarantines were announced, 34% of microenterprises stopped their livelihood. After two weeks this spiked to 51% and slightly recovered to 41% after a month of lockdown.

Some microenterprises reopened their livelihood because they need to earn income to have enough budget to buy rice at the minimum. They sourced locally-available inputs to do this and were able to sell banana cue, camote cue, cassava cake and rice cakes among others.

Majority of microenterprises or 59% reported that their livelihood weakened. Of which, 59% and 31% reported significant and severe weakening of livelihoods resepectively.

Supply chain disruption; inability to deliver goods and services; and prohibition to open non-essential businesses were the main reasons given for stopping or weakning of their livelihoods. With families having to stay home and most business remain closed, there are very few buyers of their products and services. Most barangays prohibit entry of non-residents which prevent others from going to work.

Exposure to COVID-19

An encouraging finding in the rapid community assessment is that only 2 of the 6,071 respondents are persons under monitoring. This may be a positive sign that the community quarantine is effective in containing the rapid spread of the virus.

The quarantine period was extended to April 30 and the question now is how much longer can the poor endure its negative effects to their livelihoods. Many of them are saying that they might die first of hunger before getting infected with COVID-19.

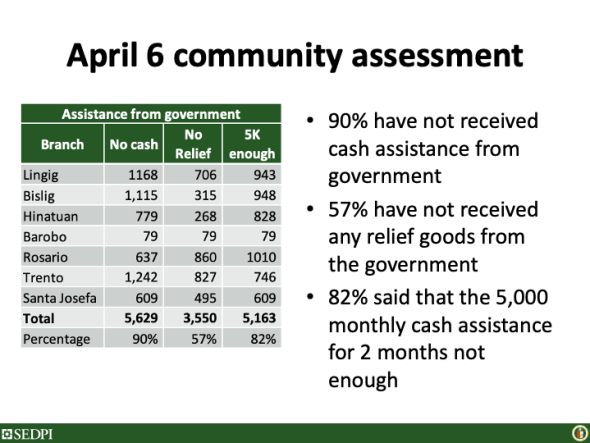

Access to government assistance

It is important to consider the well-being of low-income groups and provide them with enough economic support and social safety nets during this quarantine period. The government’s cash assistance and emergency relief is very much needed on the ground to help them survive.

Only one of ten microenterprises or 11% were able to receive cash assistance; and 60% received relief goods from the government as of April 14. This is an improvement of 1% and 17% respectively from the previous week showing marginal improvement in access to government assistance.

Those who received cash assistance got PhP3,000 to PhP4,000. Most of them received PhP3,600 cash assistance through the 4Ps program of the Department of Social Welfare and Development.

Relief goods received were composed of rice, canned goods and soap. Most of those who received these said that the supply will only last them for 1-2 days. Most of the respondents or 82% also expressed that the PhP5,000 cash assistance will not be enough to cover their daily needs in the next two months.

Recommendations during community quarantine

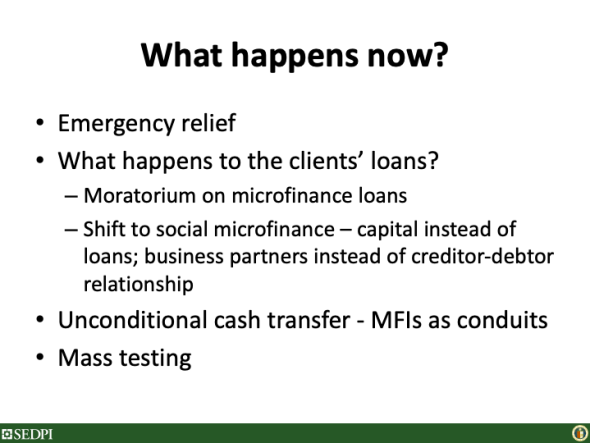

Hasten government cash assistance and relief

The government needs to hasten release of cash assistance and relief goods to microenterprises and the informal sector. These will alleviate their burden and enable them to survive the community quarantine.

Prohibit interest accrual on MSEs loans

Interest accrual for loan of micro and small enterprises during the quarantine period should be prohibited. On April 3, Ateneo-SEDPI Microfinance Capacity Building program released a position paper regarding this.

The continued charging of interest during community quarantine is socially unjust since this gives additional burden to microenterprise and small enterprises at a time when they can barely survive. This is an unnecessary additional expenses that will make their lives even harder during the rebuilding and recovery phase.

Mass testing

Prioritize mass testing to suspect and probable COVID-19 individuals who belong to low income groups, especially in urban centers, where spaces are cramped and transmission could happen faster.

Free testing services should be provided to make sure that transmission in low-income groups is prevented and managed properly. Local government units should have isolation areas for PUIs and PUMs to prevent the spread of the disease in rural and urban poor communities.

Recommendations immediately after community quarantine

The rapid community assessment showed that 77% of respondents request for cash assistance to restart their livelihood after the community quarantine. Many of the members or 35% would still need relief goods, especially food, immediately after the quarantine and A few or 12% need work to have source of income.

Cash assistance to restart livelihoods through MFIs

Request for cash assistance to restart livelihoods should be coursed through microfinance institutions (MFIs) to eliminate dole-out mentality. The cash assistance should be given, at the minimum, as 0% loans to microenterprises and the informal sector.

MFIs are well positioned to provide this intervention since they would need to support the rebooting of the livelihoods of their client base. The cash assistance will be collected alongside restructuring of existing loans of clients so that financial service delivery will continue.

Bail out MFIs

MFIs access funds from commercial banks and government financial institutions that they extend as microcredit to low income groups. Based on the Consultative Group to Assist the Poor’s (CGAP) estimate, an 85% repayment rate in MFIs would only have sufficient cshflow to last in the ext six months.

The impact of the pandemic will surely negatively impact repayment rates of MFIs. Based on the figures of those negatively affected, SEDPI estimates that it repayment rates in the next three months after the quarantine period may hit as low as 20% to 30%. Due to this, most MFIs will experience liquidity problems.

Government should intervene and infuse capital in the form of equity to MFIs to fund the proposed cash assistance intended to restart microenterprise livelihoods. Another way of doing this is to temporarily convert debt obligations of MFIs from commercial banks and especially from government financial institutions to equity to ease pressure in debt repayments.

MFIs will eventually pay this equity back to the government, perhaps event at a premium, once they recover from the crisis. SEDPI strongly suggests moving away from debt-based development assistance since interest will ultimately be passed on as additional burden to microenterprises and the informal sector.

This strategy is similar to the bailout of governments to large financial institutions during the 2008 financial crisis. If governments are willing to bail out large corporations, they should also be willing to do the same to MFIs that directly help those at the bottom of the pyramid.

Pay for work programs

Development organizations and government should provide pay-for-work programs to spur local economic development. This will create temporary employment and give purchasing power that will augment efforts to restart of livelihoods.

0% SSS and Pag-IBIG calamity loans

Microenterprises and informal sector who are members of SSS and Pag-IBIG could benefit from the calamity loans offered. Per published policy of these two organizations, members are allowed to borrow calamity loans against their personal contributions.

The interest rate for calamity loan is 5.95% for Pag-IBIG and 10% for SSS. It is highly recommended to bring the interest on the calamity loans to 0%, since these are drawn from personal contributions of members anyway.

Recommendations for the long term

Ease in access to identity documents

Access to government basic services starts with identity. The Philippine Statistics Authority should streamline processes for low-income groups to get government identification documents such as birth certificates, marriage certificates, and licenses.

Greater financial inclusion

It is also important to focus more on financial inclusion to make sure that bank accounts are opened for all low-income families so that they can easily access cash transfers and cash relief in times of disaster. This will ensure that funds truly land in the pockets of low-income groups, and could potentially reduce corruption and patronage politics.

Universal disaster insurance

It is also high time to have universal disaster insurance since the Philippines ranks high in the World Risk Index. This will make us better prepared for disasters and pandemics in the future.

The scheme will provide funds to affected communities, especially low income groups, to cope with the disaster and to rebuild livelihoods. Having disaster insurance will eliminate the need for low income groups to beg for government assistance from politicians.

Tap vast network of MFIs

Microfinance institutions are rooted well in communities and have vast networks that penetrate even the most remote areas. This makes them suitable for information dissemination as well as for distribution of government assistance.

Prioritize support and assistance to the bottom of the pyramid

We may be already enjoying the positive effect of the commuity quarantine to prevent the sudden spread of COVID-19. However, its negative economic impact especially to vulnerable sectors such as microenterprises and the informal sector, is undeniable.

To sustain and complement the gains of the quarantine, priority and free mass testing to low income groups is needed. This will hopefully flatten and at the same time shorten the curve.

Government should hasten delivery of cash and relief assistance to low income groups to alleviate the burden of low income groups. MFIs could complement barangay level legwork for information dissemination and distribution of government assistance with its vast network and penetration in rural areas.

To ease the economic burden of low income groups, the government should stay true to the intent and spirit of the Bayanihan Act, that prohibit accrual of interest and other fees during the quarantine period.

Immediately after the quarantine period, to help jumpstart the economy, the government could provide pay for work programs; and provide cash assistance to microenterprises through MFIs. It could bailout MFIs to ensure continued delivery of much needed microfinance services to the poor.

The proposed 0% calamity loans of Pag-IBIG and SSS could provide much needed relief to microenterprises and the informal sector. In the longer term, structural challenges could be addressed through providing ease in access to identity documents, broader financial inclusion, and universal disaster insurance.

When we channel resources to help microenterprises and the informal sector, we make our nation better poised to recover faster from the negative effects of COVID-19.

The COVID-19 pandemic continues to pose serious threats to health and has already disrupted the economy. This prompted the government to enact Republic Act No. 11469 otherwise known as the “Bayanihan to Heal As One Act,” declaring a state of national emergency in order respond to the urgent needs of the people.

It is in response to this urgent need and call that the Ateneo-SEDPI Microfinance Capacity Building Program (Ateneo-SEDPI MCBP) recognizes our role in aiding government to promote and protect the interests of the Filipino people, especially low income groups, in these challenging times. For the past 14 years, Ateneo-SEDPI MCBP provided training, research and consulting services to more than 2,000 microfinance institutions in the Philippines with a combined outreach of 10 million low income households.

SEDPI invests in 15 cooperatives and microfinance NGOs nationwide. It also directly provides financial services to more than 8,000 low income households in Mindanao. SEDPI works in partnership with Pag-IBIG, Social Security System, Land Bank of the Philippines and Development Bank of the Philippines to bring social protection and welfare services closer to low income groups.

Remaining true to our vision and mission, we commit to do our moral and lawful duty to provide a “grace period” for the loans of our microfinance clients.

In Section 4 (aa) of RA 11469, the law directs:

“ . . . all banks, quasi-banks, financing companies, lending companies, and other financial institutions, public and private, including the Government Service Insurance System, Social Security System and Pag-IBIG Fund, to implement a minimum of a thirty (30)-day grace period for the payment of all loans, including but not limited to salary, personal, housing, and motor vehicle loans, as well as credit card payments, falling due within the period of the enhanced Community Quarantine without incurring interests, penalties, fees, or other charges. Persons with multiple loans shall likewise be given the minimum thirty (30)-day grace period for every loan . . . ”

However, we noticed an inconsistency with the implementing rules and regulation (IRR) of RA 11469. In Section 3.01 of the IRR of RA 11469 where “Mandatory Grace Period” was discussed, it states that:

“ . . All Covered Institutions shall implement a 30-day grace period for all loans with principal and/or interest falling due within the ECQ Period without incurring interest on interest, penalties, fees and other charges. The initial 30-day grace period shall automatically be extended if the ECQ period is extended by the President of the Republic of the Philippines pursuant to his emergency powers under the Bayanihan to Heal as One Act . . . [emphasis added]”

The text of RA 11469 clearly provides in Section 4 (aa) that all loans falling due within the period of the enhanced community quarantine shall not incur interests, penalties, fees, or other charges. This provision of the law was not adhered to by the IRR when it said that “ . . . All Covered Institutions shall implement a 30-day grace period for all loans with principal and/or interest falling due within the ECQ Period without incurring interest on interest, penalties, fees and other charges . . .” [emphasis added]

Prohibiting financial institutions to impose “interest on interest” is far different from prohibiting them to impose “interest” on loans. The IRR provides that financial institutions are only mandated to cancel the additional interest that may be imposed due to late payment of the loan. This is different from what the law really provides which mandates financial institutions to totally cancel the interest of the loan for the duration of the quarantine period.

Many of our clients who have loans (microcredit) with us used this to finance their livelihood. In a community assessment we conducted on March 31, 2020, 40% of our members completely stopped their lovelihoods and another 40% reported weakened livelihoods. We were not able to reach the remaining 20% because they live in places where cellphone signal could not reach them.

This is why we, in the microfinance industry, applaud RA 11469 for canceling the interest of loans during the duration of the quarantine. In fact, as early as March 15, 2020 we already declared a moratorium on loan repayments to our clients. This means that interest on these loans for the quarantine period will not be charged.

However, if the IRR will be implemented, only “interest on interest” will be canceled and not the whole “interest” of loans during the quarantine period. This will create a huge problem for MFIs since most access loans through commercial banks. If the IRR will be implemented, MFIs will still have to pay the interest on loans from commercial banks even if MFIs already canceled the interest on the loans of our clients.

With the current IRR, MFIs will bear the brunt of the cost of interest which may endanger their financial sustainability. There is also a good chance that this interest will be passed on eventually to microfinance clients who are already bearing the biggest impact of the pandemic.

With this, we strongly urge the concerned agencies of our government – Bangko Sentral ng Pilipinas, Department of Finance and Securities and Exchange Commission – to review the IRR of RA 11469. We would like to the IRR to follow the spirit of RA 11469. Hence, we call for the revision of Section 3.01 of the IRR of RA 11469 for it to remain true to the provision of Section 4 (aa) of RA 11469.

We hope that this matter will be resolved soon. The spirit and purpose of the Bayanihan to Heal as One Act must be genuinely upheld. We call for the government to completely prohibit interest charging on loans during the enhanced community quarantine.

It is our fervent hope that this crisis will be put to an end soon. MFIs will remain a partner of the Filipino people in securing their livelihood, health, and safety all throughout this challenging times until we are able stand up again as a strong and progressive nation.

Thank you very much and may God bless our country.

In the spirit of Bayanihan and in service of the Filipino people.

His daughter, Rica Caneta, is a private school teacher. She has been helping him sell some of his works, “I made a hanging cabinet and a storage cabinet with the extra wood from the previously commissioned projects. I sold them for P2,500 and P3,000 respectively. Rica is working from home so she takes some time to promote my pieces through social media.”

His daughter, Rica Caneta, is a private school teacher. She has been helping him sell some of his works, “I made a hanging cabinet and a storage cabinet with the extra wood from the previously commissioned projects. I sold them for P2,500 and P3,000 respectively. Rica is working from home so she takes some time to promote my pieces through social media.”  Federic’s son, Drake, is an animal handler and is supporting the family through these times, “My children are providing financial support we need. Our monthly expenses are usually P10,000 which was primarily covered through my business.” He has discovered the potential of taking his business online to help it grow, “I would need around P10,000 to buy materials for future orders. Online sales have made me realize that professional guidance in promoting our business would really help it expand.”

Federic’s son, Drake, is an animal handler and is supporting the family through these times, “My children are providing financial support we need. Our monthly expenses are usually P10,000 which was primarily covered through my business.” He has discovered the potential of taking his business online to help it grow, “I would need around P10,000 to buy materials for future orders. Online sales have made me realize that professional guidance in promoting our business would really help it expand.” However, these sales do not provide stability for the pisonet.

However, these sales do not provide stability for the pisonet.  JJS Suds is a connection to the local community, “We would normally have 30 to 50 customers a day before the lockdown. We are lucky if there are five customers these days. Our daily revenue would reach up to P15,000 per day and that target is now P5,000.” John has had to cut corners to adapt to the new normal, “We had seven workers on a daily basis and now there are only two at any given time. The store is only open for limited hours because customers no longer come in late at night. It has led to slower service delivery. We have also started using electric fans.”

JJS Suds is a connection to the local community, “We would normally have 30 to 50 customers a day before the lockdown. We are lucky if there are five customers these days. Our daily revenue would reach up to P15,000 per day and that target is now P5,000.” John has had to cut corners to adapt to the new normal, “We had seven workers on a daily basis and now there are only two at any given time. The store is only open for limited hours because customers no longer come in late at night. It has led to slower service delivery. We have also started using electric fans.” Communication is a constant with John’s regular clientele. The staff coordinate with customers on Facebook. John has also decided to bring the business to his regulars, “We also support our personnel needs by helping with the laundry and delivery. The shop currently relies on delivery modality to remain operational. Finding alternative solutions is necessary to keep the business running.”

Communication is a constant with John’s regular clientele. The staff coordinate with customers on Facebook. John has also decided to bring the business to his regulars, “We also support our personnel needs by helping with the laundry and delivery. The shop currently relies on delivery modality to remain operational. Finding alternative solutions is necessary to keep the business running.” Pureza’s shop is her saving grace during the uncertainty, “We need P9,000 for our household expenses and about P7,000 for the store.” The store is a constant for her. Its history in the community mirrors Pureza’s presence and determination, “We reinvest all of our profits into the shop. I’m obtaining inventory through other channels because I want to see my store grow despite the circumstances.”

Pureza’s shop is her saving grace during the uncertainty, “We need P9,000 for our household expenses and about P7,000 for the store.” The store is a constant for her. Its history in the community mirrors Pureza’s presence and determination, “We reinvest all of our profits into the shop. I’m obtaining inventory through other channels because I want to see my store grow despite the circumstances.”

The city was distributing P2,000 for tricycle drivers which Jhun was unable to collect, “I believe it is because my house is far from the collection point. The local government did provide us with rice and sardines on two occasions. We have also received grocery items from

The city was distributing P2,000 for tricycle drivers which Jhun was unable to collect, “I believe it is because my house is far from the collection point. The local government did provide us with rice and sardines on two occasions. We have also received grocery items from  Inflation of necessary supplies during a disaster event makes business continuity an even greater challenge. Edwin’s main concern is procuring inventory, “We pick up essential ingredients from outside the local area because of lack of availability. The city’s clustering policy during the lockdown prevents vendors from sourcing some of the vegetables we need from Bukidnon.” The scarcity in supply and increase in price has forced Edwin to shut down despite being able to operate under COVID-19 safety guidelines. “The price of vegetables has inflated by 20 to 30%. Rice and grains have only gone up 10%. However, these cumulative prices make it impractical to continue operations.” The emerging caterer hopes that small businesses will receive the aid they need to carry on after the restriction, “We would appreciate logistical support, availability of supplies from the National Capital Region and other key cities, tax relief, and easing of local cluster market restrictions.”

Inflation of necessary supplies during a disaster event makes business continuity an even greater challenge. Edwin’s main concern is procuring inventory, “We pick up essential ingredients from outside the local area because of lack of availability. The city’s clustering policy during the lockdown prevents vendors from sourcing some of the vegetables we need from Bukidnon.” The scarcity in supply and increase in price has forced Edwin to shut down despite being able to operate under COVID-19 safety guidelines. “The price of vegetables has inflated by 20 to 30%. Rice and grains have only gone up 10%. However, these cumulative prices make it impractical to continue operations.” The emerging caterer hopes that small businesses will receive the aid they need to carry on after the restriction, “We would appreciate logistical support, availability of supplies from the National Capital Region and other key cities, tax relief, and easing of local cluster market restrictions.” Keeping their office is the biggest challenge, “Our maintenance cost fluctuates between P5,000 to P10,000 and the rental fee for the office is P7,000. We have used our savings to continue paying the rent and any vehicle maintenance that was necessary.” Shirly also has to consider the family expenses, “My sister works in Hong Kong and has sent us remittance of P20,000 during the lockdown. We were able to use the money for four months of household expenses. If we can resume operations soon, we would only need P5,000 to start functioning again.”

Keeping their office is the biggest challenge, “Our maintenance cost fluctuates between P5,000 to P10,000 and the rental fee for the office is P7,000. We have used our savings to continue paying the rent and any vehicle maintenance that was necessary.” Shirly also has to consider the family expenses, “My sister works in Hong Kong and has sent us remittance of P20,000 during the lockdown. We were able to use the money for four months of household expenses. If we can resume operations soon, we would only need P5,000 to start functioning again.” Multiple income-generating opportunities are a proven solution for many small businesses to sustain their needs. The COVID-19 restrictions have limited these prospects to entrepreneurs. Giselle currently works as a cashier for a university. It is the only stable income for the household. The lack of earnings has forced her to take loans, “My husband has a van that he would use for delivery operations. He would regularly work for Lazada but that has also stopped since March.” Loss of revenue sources has multifold consequences for microentrepreneurs. “We have lost around P19,000 a month since the lockdown. We also had an SUV that we would rent out through the Grab app. Unfortunately, we had to give it back to the dealership because we were unable to cover the monthly payment or the driver’s salary.”

Multiple income-generating opportunities are a proven solution for many small businesses to sustain their needs. The COVID-19 restrictions have limited these prospects to entrepreneurs. Giselle currently works as a cashier for a university. It is the only stable income for the household. The lack of earnings has forced her to take loans, “My husband has a van that he would use for delivery operations. He would regularly work for Lazada but that has also stopped since March.” Loss of revenue sources has multifold consequences for microentrepreneurs. “We have lost around P19,000 a month since the lockdown. We also had an SUV that we would rent out through the Grab app. Unfortunately, we had to give it back to the dealership because we were unable to cover the monthly payment or the driver’s salary.”

Two months after the government started easing lockdowns in most parts of the country, 36% of nanoenterprises reported to have bounced back to pre-pandemic level. In May, only 18% expected to bounce back within one month which may be a good sign of recovery if the spread of the virus is contained.

Two months after the government started easing lockdowns in most parts of the country, 36% of nanoenterprises reported to have bounced back to pre-pandemic level. In May, only 18% expected to bounce back within one month which may be a good sign of recovery if the spread of the virus is contained.

With microenterprises cautious on demand, they prefer not to access loans. Only two of three of those who finished their loans opted to renew their for another cycle. This is also a sign that nanoenterprise have the ability to weigh risks and returns.

With microenterprises cautious on demand, they prefer not to access loans. Only two of three of those who finished their loans opted to renew their for another cycle. This is also a sign that nanoenterprise have the ability to weigh risks and returns. There are approximately 8 million low income households that access microfinance services in the Philippines. MFIs are frontliners in the delivery of financial services to low income groups who find it difficult to open deposit accounts and access loans from commercial banks.

There are approximately 8 million low income households that access microfinance services in the Philippines. MFIs are frontliners in the delivery of financial services to low income groups who find it difficult to open deposit accounts and access loans from commercial banks.

Agrarian Reform Beneficiary Organizations (ARBO) in Sarangani, Sultan Kudarat, Maguindanao, and Lanao del Sur Provinces remain covid free. This is the result of the ARBO covid-19 quick assessment conducted by SEDPI on April 20-24, 2020.

Agrarian Reform Beneficiary Organizations (ARBO) in Sarangani, Sultan Kudarat, Maguindanao, and Lanao del Sur Provinces remain covid free. This is the result of the ARBO covid-19 quick assessment conducted by SEDPI on April 20-24, 2020.

The rapid community assessment showed that 77% of respondents request for cash assistance to restart their livelihood after the community quarantine. Many of the members or 35% would still need relief goods, especially food, immediately after the quarantine and A few or 12% need work to have source of income.

The rapid community assessment showed that 77% of respondents request for cash assistance to restart their livelihood after the community quarantine. Many of the members or 35% would still need relief goods, especially food, immediately after the quarantine and A few or 12% need work to have source of income.